Cole-Frieman & Mallon Presenting a Digital Asset Legal Update for 2020

We are excited to present our first webinar to update the industry on the various updates applicable to digital asset managers. We will be providing the US legal update during the webinar and will be covering the following topics:

Proposed Laws (state and federal)

Wyoming Update

SEC Digital Asset Priorities

The Courts

Structuring Trends

Below is our invitation for the event – it is free to join and all are welcome. Look for coming posts providing an overview of the content from the webinar. As always, please contact us if you’d like to be added to any mailing lists.

****

With the rescheduling of our 2020 CoinAlts Fund Symposium to Fall of 2021, we are excited to announce our new CoinAlts Webinar Series, beginning on Thursday, May 14th at 11:00am PT.

Hear from industry experts on the investment, legal and operational issues that digital asset managers are facing in today’s climate.

After the panel, we are excited to host a Q&A session with Matt Perona from Polychain Capital.

If you would like to submit a question for consideration to one of the founding sponsors or Matt Perona, you will have the opportunity to do so upon registration. For those unable to join, the webinar will be available for replay within 24 hours.

We look forward to having you!

All the best,

Cole-Frieman & Mallon LLP

****

Bart Mallon is a founding partner of Cole-Frieman & Mallon LLP. Cole-Frieman & Mallon is a boutique law firm focused on providing institutional quality legal services to the investment management industry. For more information on this topic, please contact Mr. Mallon directly at 415-868-5345.

The first quarter of

2020 saw an unprecedented combination of challenges, not only industry-wide but

on a global scale as well. Notwithstanding the prevailing circumstances, the

first quarter was busy for investment managers and service providers with

filing deadlines, regulatory changes, and compliance updates. As we continue

through 2020, we have put together this update and checklist to help managers

stay on top of the business and regulatory landscape in consideration of the

global pandemic affecting nearly every aspect of the industry and our

lives.

Please note COVID-19 related matters appear at the end of this update.

****

SEC

Matters

SEC Releases 2020

Examination Priorities. The SEC Office of Compliance Inspections and

Examinations (“OCIE”), which conducts examinations of SEC-registered

investment advisers, investment companies, broker-dealers, and others,

publishes an annual

list of examination priorities for

the upcoming year that provides insight to managers regarding issues that will

be examined and an opportunity for advisers to prepare and improve such areas

before examination.OCIE’s 2020 exam priorities are as follows: Retail

Investors (including seniors and those saving for retirement); Market

Infrastructure; Information Security; Focus Areas Relating to Investments

Advisers, Investment Companies, Broker-Dealers, and Municipal Advisors;

Anti-Money Laundering Programs; Financial Technology and Innovation (including

Digital Assets and Electronic Investment Advice); and oversight of the

Financial Industry Regulatory Authority (FINRA) and Municipal Securities

Rulemaking Board (MSRB). In particular, Information Security and Cybersecurity

were focuses of the publication. OCIE released observations that focus on certain

approaches taken by market participants in regards to governance and risk management,

access rights and controls, data loss prevention, mobile security, incident

response and resiliency, vendor management, and training and awareness.

SEC Division of Trading and Markets Releases FAQ on Regulation Best Interest (Reg BI). Reg BI establishes a “best interest” standard for broker-dealers and associated persons when making recommendations to retail customers involving securities. Since adopting Reg BI on June 5, 2019, the SEC has released responses to frequently asked questions about the regulation, covering topics surrounding Retail Customers, Recommendations, Disclosure Obligations, Care Obligations, Conflict of Interest Obligations, and Compliance Obligations. It should be noted that like all staff guidance, the FAQ does not have legal force or effect, but represents the views of the staff of the Division of Trading and Markets. Reg BI was met with much skepticism as critics found the new regulation ambiguous in many regards. Hopefully the SEC’s guidance will be the first step in addressing this perceived ambiguity. Firms are expected to comply with Reg BI by June 30, 2020.

****

FINRA

Matters

Amendments to the

FINRA New Issue Rule (Rule 5130) and Anti-Spinning Rule (Rule 5131) Became

Effective as of January 1, 2020. Generally, the amendments to the FINRA New

Issue Rules broaden the types of investors that are exempt from the rules’

restrictions and narrow the types of the securities offerings that are subject

to the New Issue Rules. As a result of the amendment, among other things, FINRA

member broker-dealers may now sell new issues to additional kinds of investors

directly or through investments in private investment funds. Amendment to Rules

5130 and 5131 includes expanding the ways that foreign investment companies can

fall within the general exemption, broadening the definition of family

investment vehicles, including foreign employee retirement benefits plans under

the exemption, excluding sovereign entities from the definition of “Restricted

Persons,” and other changes.

FINRA Releases 2020 Risk Monitoring and Examination Priorities Letter. The 2020 Risk Monitoring and Examination Priorities Letter outlines the priorities for FINRA’s risk monitoring, surveillance, and examination programs for the year. The letter includes a list of practical considerations and questions for firms to use as guidance in evaluating their compliance, supervisory, and risk management program. Among the new or emerging areas in the industry, FINRA discusses compliance with obligations relating to Regulation BI, Form CRS, communications with the public, communications via digital channels, sales of initial public offering (IPO) shares, digital assets, cybersecurity, and other items.

****

Digital

Asset Matters

SEC Commissioner

Proposes 3-Year Safe Harbor Period for Crypto Token Sales. As

mentioned in Commissioner Peirce’s speech, cryptocurrency and

digital asset entrepreneurs are faced with a regulatory Catch 22. In order to

build a decentralized network in which a token provides access to a function of

the network or serves as a means of exchange, a crypto project needs to get its

tokens into the hands of users. However, such would-be networks generally

cannot freely distribute their tokens to potential users due to existing

federal and/or state securities laws. Consequently, these would-be networks

cannot mature into functional decentralized networks that are not dependent

upon single persons or groups to carry out the essential managerial or

entrepreneurial efforts (under the Howey Test). To address this

uncertainty, Commissioner Peirce formally proposed a safe harbor for token

projects, allowing a three-year time window for networks to mature and become

sufficiently decentralized so as not to fall under the “securities” definition

contemplated under the Howey Test. If adopted, the safe harbor

would impose strict requirements on such crypto projects, including source code

disclosures, transaction history disclosures, personal disclosures, public

notices and filings, and other conditions. Additionally, the safe harbor would

be available for tokens that were previously sold in a registered offering or

pursuant to a valid exemption under the Securities Act of 1933, as

amended.

SEC Wins Injunction

against Telegram in Landmark Digital Assets Case. On

March 24, U.S. District Judge Kevin Castel of the Southern District Court of

New York issued an injunction against

Telegram Group Inc. (“Telegram”), the messaging app company that raised $1.7

billion in 2018 selling Gram tokens to investors in the largest ICO to date. In

October 2019, the SEC

sought to enjoin Telegram from

distributing the Gram tokens on the grounds that the company had violated

federal law for the sale of unregistered securities. The SEC was granted the

preliminary injunction, preventing Telegram from distributing the Gram tokens

to investors. The Court stated it “finds that the delivery of Grams to the

Initial Purchasers, who would resell them into the public market, represents a

near certain risk of a future harm, namely the completion of a public

distribution of a security without a registration statement.” Despite the

ruling, it has been reported that the Telegram Open Network (TON) Community

Foundation remains optimistic as they believe that TON can always be launched

by anyone considering the network code is available.

Crypto Crash Leads to

BitMEX Outage, Liquidations. As the price of

Bitcoin crashed from $8,000 to nearly $3,700 in less than 24 hours on March 13,

BitMEX faced

a 25 minute outage during a day when nearly $1 billion in leveraged long

positions were liquidated industry-wide. BitMEX has faced criticism for the

outage, with some speculating that it may have shut down intentionally to avoid

the possibility of its Bitcoin perpetual swap collapsing to zero due to forced

liquidations. BitMEX has stated that a hardware issue caused the outage. No

matter the cause, this event highlights the necessity for digital asset

managers, especially those using leverage to trade digital assets, to ensure

their fund documents contain the necessary disclosures regarding counterparty

risk and digital asset exchange risks.

Wyoming Plans to Create New Bank Dedicated for Digital Assets. Wall Street and crypto veteran Caitlin Long recently announced a plan for Wyoming corporation, Avanti Financial Group Inc., to apply for a bank charter under Wyoming’s special-purpose depository institution law. Under the name “Avanti Bank & Trust,” the future bank is partnering with Blockstream to provide payment, custody, securities, and commodities activities for institutional customers using digital assets (“Avanti”). Though Avanti has yet to submit the bank charter application, the company has raised $1 million in seed funding and has eight products in the works that are not currently available in the U.S. market, including custody for security tokens. If successful, Avanti will be the first U.S. bank dedicated for digital assets.

****

Offshore

Matters

Cayman Islands Mutual

Funds Law (2020 Revision). Effective February 7, 2020, the Cayman Islands

Government enacted an amendment to the Mutual Funds Law (2020 Revision).

The 2020 Revision requires registration of previously exempt Section 4(4) Funds

(generally, private funds with not more than 15 investors) with the Cayman

Island Monetary Authority (“CIMA”). The 2020 Revision operates retroactively,

meaning mutual funds that were previously exempted from registration under

Section 4(4) will now need to comply with the registration requirements by

August 7, 2020. Registration is similar to the requirements for Section 4(3)

Funds, including the ‘four-eyes’ principle that necessitates funds to have at

least two natural persons in management roles.

Cayman Islands Private

Funds Law 2020 (“PF Law”). Effective February 7, 2020 (the “Effective

Date”), the PF Law

requires any Cayman Islands closed-ended fund that falls under the definition

of a “private fund” to register with CIMA. Previously, “private funds” were not

required to register with CIMA. A vehicle will be a “private fund” where: (1)

its principal business is offering and issuing investment interests; (2) its

investment interests carry an entitlement to participate in the profits or

gains of the vehicle and are not redeemable or re-purchasable at the option of

the investor, i.e. are closed-ended; (3) its purpose or effect is the pooling

of investor funds with the aim of spreading investment risks and enabling

investors to receive profits or gains from such vehicle’s investments; (4) the

investors do not have day-to-day control over the investments; (5) its

investments are managed as a whole by or on behalf of the operator, directly or

indirectly, for reward based on the assets, profits or gains of the vehicle;

and (6) it does not constitute a “non-fund arrangement,” as listed in the

schedule to the PF Law. The regulations do provide certain transitional

provisions for private funds that began business at any time prior to the

Effective Date. Such transitional funds will have six months from the Effective

Date to register with CIMA and comply with the PF Law.

European Union (EU) Announces Cayman Islands is a Non-Cooperative Jurisdiction for Tax Purposes. Effective February 18, 2020, the EU Economic and Financial Affairs Council announced that the Cayman Islands was moved to Annex 1 of Non-cooperative jurisdictions (“Annex 1”) for failing to timely implement appropriate regulations relating to economic substance in the area of collective investment vehicles. For investors or clients using Cayman structures, the move to Annex 1 will have limited or no direct practical consequence. The move to Annex 1 is not expected to trigger prevention of the use of special purpose vehicles established in non-EU jurisdictions under Article 4 of the EU Securitisation Regulation, or result in any EU level sanctions. While the Cayman Islands Government has announced the start of the delisting process, the situation is currently being monitored as dialogue continues between the EU and listed jurisdictions.

****

Other

Matters

Important Second Circuit Opinion on Insider Trading. In United States v. Blaszczak, No. 18-2825 (2d Cir. Dec. 30, 2019) (“Blaszczak”), the Second Circuit denied application of any personal benefit test to insider trading charges brought under both the criminal securities fraud provisions added in the 2002 Sarbanes-Oxley Act (Title 18) and the wire fraud statutes. Although this precedent controls only in criminal cases, this Second Circuit decision has made it significantly easier for prosecutors to obtain insider trading convictions. The personal benefit test requires prosecutors to show that a tipper acquired a personal benefit by disclosing confidential information in order to charge the tipper or tippee with insider trading. The implications of the ruling are potentially far-reaching as Blaszczak may become expansive precedent for prosecutors seeking to lower the bar for insider trading prosecutions. Analysts, such as the two former hedge fund analysts to whom Blaszczak was charged, that usually communicate with company employees and executive insiders may be at higher risk for insider trading prosecution because the government may not need to allege or prove that the tipper breached a duty of confidentiality or exchange for a personal benefit. While the cascading impact following Blaszczak is yet to be known, it is clear that the Second Circuit ruling has the potential to significantly expand insider trading liability.

****

COVID-19

Pandemic-Related Updates

SEC Regulatory Relief

for Funds and Investment Advisers Affected by COVID-19. The

SEC

announced it will provide conditional relief to

investment advisers affected by COVID-19. TheSEC order grants relief for

advisers from certain Form ADV and Form PF filing obligations. Registered

investment advisers (“RIAs”) and exempt reporting advisers affected by COVID-19

can expect conditional relief regarding amendments and reports on Form ADV,

respectively. Further, the order provides conditional relief for RIAs affected

by COVID-19 in regards to delivering amended brochures, brochure supplements or

summaries of material changes to clients where the disclosures are not able to

be timely delivered. Private fund advisers affected by COVID-19 can also expect

relief from Form PF filing requirements. To rely upon the relief, the order

requires a statement of notification to Commission staff (promptly via email to

the SEC at [email protected])

of the intention to rely upon the order and the disclosure of information in

the form of a brief description by the adviser of the reasons why it could not

file or deliver its Form ADV or Form PF on time. Clients and investors of the

adviser must also be notified. Disclosure in regards to reliance upon the order

for Form PF filings should be made promptly via email to the SEC at [email protected].

The order requires filing Form ADV and/or Form PF, as applicable, as soon as

practicable, but not later than 45 days from the original deadline. For general

questions or concerns related to impacts of coronavirus on the operations or

compliance of funds and advisers, please contact us.

California’s Attorney

General Announced No Delay on Enforcement of CCPA. On

March 17, a group of over 30 trade associations and businesses sent a letter to

California’s Attorney General pushing to postpone the enforcement of the California Consumer Privacy Act

(“CCPA”). The CCPA, which took effect on January 1, is expected to be enforced

by the Attorney General starting July 1. The group who sent the letter

requested a January 1, 2021 enforcement date in order to give businesses more

time to prepare for enforcement given that, given the current climate of

COVID-19, many are unable to prepare for enforcement and most are in need of

prioritizing other business concerns, such as the well-being and health of

their employees. Press reports of various statements by members of the Attorney

General’s office in response to this request strongly suggest that enforcement

will not be delayed. In addition, the Attorney General recently released

proposed revisions to clarify the service provider exemption. One such revision

would allow service providers to use personal information internally to improve

their services subject to certain limitations. Nevertheless, fund managers

should prepare for enforcement of the CCPA as scheduled.

Investment Management

Firms May Be Considered Essential Financial Businesses Under Federal Guidance

and State Orders. The Cybersecurity and Infrastructure Security

Agency (“CISA”) lists asset management as

a vital component of our nation’s critical infrastructure. As the federal risk

advisor, CISA created guidance to help state and local governments ensure that

employees essential to operations are able to continue working. In

consideration of CISA’s guidance, whether or not investment management firms

would be considered essential financial businesses may depend upon each State’s

directives. Generally, the best practice for firms moving forward is to require

workers to telework or work-from-home if possible, but allow supporting

personnel to continue selective operations in the office in order to ensure the

firm’s continued operation.Please read here for a state-by-state

analysis of the exceptions provided in each States’ executive orders regarding

essential business activities in light of the COVID-19 public emergency

response.

Amidst Extreme

Volatility Managers Must Assess Material Terms in Live Trading Agreements.

Given extreme market volatility, managers must assess the deal terms governing

trading agreements such as ISDA master agreements, prime brokerage agreements,

and others as certain provisions and triggering events may detrimentally affect

hedge funds in the midst of

current market conditions. Provisions regarding NAV triggers, force

majeure, material adverse change/effect, counterparty powers, business day

determinations, business disruptions, etc. and should be reviewed in light of

current market conditions. In particular, for fund managers with ISDAs in

place, please read this article by Dave Rothschild, a

Partner at Cole-Frieman & Mallon LLP (“CFM”).

Additional Information

on COVID-19 for Investment Managers. We have

summarized a number of items from various authorities that pertain to

investment managers. This article details the following

matters:

The Coronavirus Aid, Relief, and Economic Security Act (CARES Act).

CFTC Extended Deadlines for CPOs Due to COVID-19.

SEC Update to Form ADV and Custody Rule FAQs, Relating to “Work From Home”.

NFA Relief for Commodity Pool Operators, Relating to “Work from Home”.

FINRA Pandemic-Related BCP, Guidance and Regulatory Relief, Relating to Regulatory Filings, “Work from Home,” Cybersecurity, and Forms U4 and BR.

Employment Considerations for Investment Management Firms Addressing COVID-19.

SEC Temporary Final Rule 10(c) to Address Form ID Notarization Issues.

SEC’s Office of Compliance Inspections and Examinations Off-Site Exams via Correspondence for Information on Firms’ Business Continuity Plans.

SEC Guidance Relating to Federal Proxy Rules for Annual Meetings, “Virtual” Meetings, and Presentations of Shareholder Proposals.

SEC No-Action Relief for Consolidated Audit Trail Obligations.

Short-Selling Bans in Austria, Belgium, France, Italy, and Spain.

Tax Matters for Investment Managers.

****

CFM

Events

CFM 2020 IA/BD

Compliance Update with Aspect Advisors. We held our

2020 compliance update with Aspect Advisors in January. The discussion covered the critical

compliance priorities in our industry for the New Year and decade. We’d

like to thank Aspect Advisors

for their help with this compliance update and look forward to future

events. Aspect Advisors is a modern regulatory consultant providing

customized compliance solutions to entrepreneurs. The firm has a focus on

fintech companies, broker-dealers, and investment managers (hedge fund, VC, PE,

RIA, etc.).

Bitcoin Mining Panel

Event in San Francisco. As we have seen certain venture capital

firms increase their investment in bitcoin mining and infrastructure, CFM

decided to hold an event discussing the current investing environment,

regulatory considerations, and infrastructure landscape for bitcoin mining. The

discussion was presented by Michael Fitzsimmons of Williams Trading and

featured a panel of bitcoin mining experts – Mathew D’Souza of Blockware

Solutions, Thomas Ao of MCredit and Yida Gao of Struck Capital. For a summary

of the event, please see our overview.

Regulation Best Interest (Reg BI) Webinar. Please stay tuned for more information on an upcoming live webinar, co-sponsored by CFM and Aspect Advisors, discussing practical, regulatory, and other considerations regarding Reg BI and the new Form CRS. We have previously written about Reg BI and how it pertains to private fund managers and investment advisers here. If you are interested in attending and have any questions for us to cover during the webinar, please contact us.

Compliance Calendar Please note the following important dates as you plan your regulatory compliance timeline for the coming months:

Deadline

Filing

March 30

SEC deadline to update and file Form ADV – Part 1A, 2A, and Part(s) 2B, as applicable, through IARD.

April 10

Amendment to SEC Form 13H due if necessary.

April 15

SEC deadline to file 1st Quarter 2020 Form PF filing for quarterly filers (Large Liquidity Fund Advisers), through PFRD.

April 15

FinCEN deadline to file Report of Foreign Bank and Financial Accounts on FinCEN Form 114. Required for U.S. person with financial interest in, or signature authority over, one or more foreign financial accounts with total value over $10,000 at any time in 2019.

April 29

Distribute Form ADV Part 2 to existing clients.

April 29

Distribute audited financial statements to private fund investors that have not invested in fund of funds.

April 29

SEC deadline to file Annual Form PF for annual filers (Large Private Equity Fund Advisers and Smaller Private Fund Advisers).

April 29

Collect quarterly Transaction Reports from access persons for their personal securities transactions.

May 1

SEC filing opens for Form CRS, through IARD.

May 15*

CFTC deadline for Commodity Pool Operators to file Schedules A and B of CFTC Form CPO-PQR, through NFA EasyFile.

NFA deadline for CFTC-registered CPO of CFTC Regulation 4.7 Pool or Non-Exempt Pool to file 2019 Annual Report and distribute to pool participants.

May 15

SEC deadline to file Form 13F for first quarter of 2020.

May 15

NFA deadline to file Quarterly Commodity Trading Advisor Form PR filing, through NFA EasyFile.

May. 29

SEC deadline to file 1st Quarter 2020 Form PF filing for quarterly filers (Large Hedge Fund Advisers), through PFRD.

May 29

CFTC deadline for Commodity Pool Operators to file Schedules A, B, and C of CFTC Form CPO-PQR, for first quarter of 2020, through NFA EasyFile.

May 29

CFTC deadline for Commodity Pool Operators to file NFA Form PQR for first quarter of 2020 with CFTC and NFA, through NFA EasyFile.

June 12*

Distribute Quarterly NAV Report (registered commodity pool operators claiming the 4.7 exemption) to pool participants.

June 26

Distribute audited financial statements to private fund investors that have invested in fund of funds.

June 30

SEC deadline to file Form CRS, through IARD if necessary.

Variable

Distribute copies of K-1 to fund investors.

Periodic FIlings

Form D and Blue Sky filings should be current.

*Extended deadline pursuant to COVID-19 pandemic-related relief

Please contact us with any questions or for assistance with any of the above topics. Sincerely, Karl Cole-Frieman, Bart Mallon, Lilly Palmer, David Rothschild, & Scott Kitchens

****

Cole-Frieman & Mallon LLP is a premier boutique investment management law firm, providing top-tier, responsive, and cost-effective legal solutions for financial services matters. Headquartered in San Francisco, Cole-Frieman & Mallon LLP services both start-up investment managers, as well as multi-billion-dollar firms. The firm provides a full suite of legal services to the investment management community, including hedge fund, private equity fund, venture capital fund, mutual fund formation, adviser registration, counterparty documentation, SEC, CFTC, NFA and FINRA matters, seed deals, hedge fund due diligence, employment and compensation matters, and routine business matters. The firm also publishes the prominent Hedge Fund Law Blog, which focuses on legal issues that impact the hedge fund community. For more information, please visit us at colefrieman.com.

****

Bart Mallon is a founding partner of Cole-Frieman & Mallon LLP. Cole-Frieman & Mallon is a boutique law firm focused on providing institutional quality legal services to the investment management industry. For more information on this topic, please contact Mr. Mallon directly at 415-868-5345.

Below is our compilation of communications that are relevant to investment managers. Please let us know if you are looking for additional information and we will strive to update this as time goes on. Stay safe and sane – CFM 4/14/20

****

The Coronavirus Aid, Relief, and Economic Security Act (CARES Act). On March 27, Congress passed the $2 Trillion CARES Act, the largest financial relief bill in history, aimed at providing financial assistance to businesses and individuals to alleviate the economic fallout caused by the COVID-19 public health crisis. A core focus of the CARES Act is $350 billion in financial aid for small businesses through federal loans under a new Small Business Administration (“SBA”) loan program called the Paycheck Protection Program (the “PPP”). Here is our post on highlights of the program in regards to financial relief for small businesses.

SEC Regulatory Relief for Funds and Investment Advisers Affected by COVID-19. The SEC announced it will provide conditional relief to investment advisers and investment funds affected by COVID-19. In particular, the SEC order grants relief for investment advisers from certain Form ADV and Form PF filing obligations. Disruptions caused by COVID-19 to transportation, access to facilities, support staff and the ability for gatherings, among other things, may prevent or delay investment advisers and investment funds from meeting regulatory obligations. As a result, registered investment advisers (“RIAs”) and exempt reporting advisers (“ERAs”) affected by COVID-19 can expect conditional relief regarding the filing of amendments to Form ADV and reports on Form ADV part 1A, respectively. Further, the order provides conditional relief for RIAs affected by COVID-19 in regards to delivery of amended brochures, brochure supplements or summaries of material changes to clients where the disclosures are not able to be timely delivered. Private fund advisers affected by COVID-19 can also expect relief from Form PF filing requirements. For an entity seeking reliance upon the conditional relief, the SEC order requires a statement of notification to Commission staff (promptly via email to the SEC at [email protected]) of the intention to rely upon the order and the disclosure of information in the form of a brief description by the adviser of the reasons why it could not file or deliver its Form ADV or Form PF on time. Clients and investors of the adviser must also be notified. Disclosure in regards to reliance upon the order for Form PF filings should be made promptly via email to the SEC at [email protected]. The order requires filing Form ADV and/or Form PF, as applicable, as soon as practicable, but not later than 45 days from the original deadline. The Commission and the staff are continuing to assess the impacts and will be considering further relief designed to help funds and advisers to continue operations and meet regulatory deadlines. For general questions or concerns related to impacts of coronavirus on the operations or compliance of funds and advisers, please contact us.

CFTC Extended Deadlines Due to COVID-19. The CFTC has extended deadlines for Commodity Pool Operators (“CPOs”) in light of recent world events, most notably the COVID-19 global pandemic. The extensions only apply to CPOs which have reporting obligations, generally this means fully registered CPOs and those subject to Rule 4.7 relief. Moreover, these extensions only apply to CPOs “where compliance is anticipated to be particularly challenging or impossible because of displacement of registrant personnel from their normal business sites…in response to the COVID-19 pandemic.” The extension applies to (i) Form CPO-PQR where small and mid-size filers must file their annual Form CPO-PQR by May 15, 2020 and large filers (who were already expected to deliver the annual Form CPO-PQR) may file their Q1 2020 Form CPO-PQR by July 15, 2020; (ii) Pool annual reports under CFTC Rule 4.7(b)(3) and 4.22(c), such annual reports were originally due on April 30, 2020 but the extension allows CPOs to deliver these annual reports to the NFA and pool participants no later than 45 days after the original due date of April 30, 2020 (note: CPOs may also seek up to an additional 180 days from the end of their fiscal year to file under the “hardship” provisions of CFTC Rule 4.22(f); and (iii) Periodic account statements under Commission Regulations 4.7(b)(2) or 4.22(b), these monthly or quarterly reports for periods ending on or before April 30, 2020 may be delivered to pool participants within 45 days after the end of the reporting period. Such relief by the CFTC is not without conditions – if CPOs do indeed rely on such extensions they must: (i) Establish and maintain a sufficient supervisory system reasonably designed to supervise the activities of personnel while working from alternative or remote locations during the COVID-19 pandemic; and (ii) return to ordinary compliance with all CFTC rules covered by the relief as the COVID-19 pandemic abates. Moreover, CPOs should thoroughly document the activation and application of any relevant business continuity policy in response to COVID-19 as the matter could easily become an item of interest on future NFA exams.

Investment Management Firms May Be Considered Essential Financial Businesses Under Federal Guidance and State Orders. The Cybersecurity and Infrastructure Security Agency (CISA) lists asset management as a vital component of our nation’s critical infrastructure. As the federal risk advisor, CISA created guidance to help state and local governments ensure that employees essential to operations are able to continue working. In consideration of CISA’s guidance, whether or not investment management firms would be considered essential financial businesses may depend upon each State’s directives. Generally, the best practice for firms moving forward is to require workers to telework or work-from-home if possible, but allow supporting personnel to continue selective operations in the office in order to ensure the firm’s continued operation.Please see our post for a state-by-state analysis of the exceptions provided in each States’ executive orders regarding essential business activities in light of the COVID-19 public emergency response.

SEC Update to Form ADV and Custody Rule FAQs, Relating to “Work From Home”. Two circumstances are at the forefront of this update, where 1) advisers might otherwise be required to identify home offices as places of business on the Form ADV; and 2) advisers may inadvertently receive securities from clients at an office location at which the advisers’ personnel may not have access to mail or deliveries. In regards to the first circumstance, the SEC FAQ indicates it would not take action against advisers who do not update Item 1F of Part 1A or Section 1F of Schedule D of their Form ADVs to represent remote/home offices from which employees are working as additional offices, unless the remote office arrangement (other than one’s principal office and place of business) is unrelated to the firm’s business and continuity plan. In regards to the second circumstance, under the Custody Rule, an investment adviser that inadvertently receives client funds or securities are required to return such securities to the client within three to five business days; otherwise, such adviser may be deemed to have custody of such securities. The SEC has revised the Custody Rule such that client assets are not considered received until firm personnel are able to access the mail or deliveries. As with most conditional relief provided by the SEC in light of COVID-19, the adviser must be unable to access mail or deliveries as a result of the circumstances caused by COVID-19.

NFA Relief for Commodity Pool Operators, Relating to “Work from Home”. Commodity pool operators (“CPO”), commodity trading advisors (“CTA”), and other NFA members implementing contingencies pursuant to their business continuity plans that permit employees, including registered Associated Persons (“APs”), to work from home, will not be subject to disciplinary action relating to the requirements that firms list as a branch office on its Form 7-R any location other than the main business address and that each branch office must have a branch office manager in compliance with Rule 2-7 that requires successful completion of the Series 30, Branch Manager Examination. The relief requires that the CPO or CTA implement and clearly document alternative supervisory methods and activities, especially surrounding recordkeeping requirements.

FINRA Pandemic-Related BCP, Guidance and Regulatory Relief, Relating to Regulatory Filings, “Work from Home”, Cybersecurity, and Forms U4 and BR. Member firms experiencing complications resulting from COVID-19 should contact their Risk Monitoring Analysists or relevant FINRA department to seek extensions. FINRA may waive late fees and provide conditional relief based on the member firm’s circumstances. As discussed earlier, firms are reminded to review, revaluate, and update their BCPs in consideration of pandemic preparedness. FINRA member firms are encouraged to contact their assigned FINRA Risk Monitoring Analyst to discuss the implementation of their BCPs, as well as challenges in such implementation, including disruption of business operations. In regards to remote offices or telework arrangements, FINRA expects member firms to maintain a supervisory system that is designed to supervise the activities of each associated person working remotely. FINRA further recommends steps to reduce the risk of a cybersecurity breach, including: “(1) ensuring that virtual private networks (VPN) and other remote access systems are properly patched with available security updates; (2) checking that system entitlements are current; (3) employing the use of multi-factor authentication for associated persons who access systems remotely; and (4) reminding associated persons of cybersecurity risks through education and other exercises that promote heightened vigilance.” In regards to Form U4/Form BR, FINRA is temporarily suspending the requirements to update Form U4 information about office employment addresses for registered persons and Form BR information regarding branch office applications for any newly opened temporary office location or space-sharing arrangements. Additionally, if a member firm relocates personnel to a temporary location that is not currently registered as a branch office, the firm must provide written notification to its FINRA Risk Monitoring Analyst. The notification should indicate at minimum the office address, the names of the member firms involved, the names of registered personnel, a contact telephone number, and expected duration, if possible.

Employment Considerations for Investment Management Firms Addressing COVID-19. With the spread of COVID-19, many employers are concerned about the health and safety of their employees and evaluating the steps that should be taken in response. We recommend that managers establish policies and procedures regarding COVID-19 and to ensure that any policies and procedures are uniformly applied, to avoid the risk of employee discrimination. If any employees exhibit flu-like symptoms, employers may ask such employees if they would like to seek medical attention and may require symptomatic employees to go home without violating the American Disabilities Act. If an employee’s condition could pose a “direct threat”, i.e. a significant risk of substantial harm to the health and safety of the individual or others that cannot be eliminated or reduced by reasonable accommodation, employers may also request that an employee be tested for COVID-19. If an employee tests positive for the virus, all employees who were in close contact with such employee should be sent home for a 14-day self-monitoring period, and other employees in the same work location should be informed of their potential exposure. As a reminder, employers should always ensure the confidentiality of employee medical information. As many workplaces shift to remote working, employers should make certain that their policies address the provision and proper use of technologies necessary for remote work. Managers should be especially careful to ensure adequate controls and safeguards are in place to protect confidential or sensitive information, particularly client information. Managers with questions policies and practices to address COVID-19 should speak with their firm’s outside counsel.

California’s Attorney General Pressed to Postpone Enforcement of CCPA. On March 17, a group of over 30 trade associations and businesses sent a letter to California’s Attorney General pushing to postpone the enforcement of the California Consumer Privacy Act (“CCPA”). The CCPA, which took effect on January 1, is expected to be enforced by the Attorney General starting July 1. The group who sent the letter requested a January 1, 2021 enforcement date in order to give businesses more time to prepare for enforcement given that, given the current climate of COVID-19, many are unable to prepare for enforcement and most are in need of prioritizing other business concerns, like the well-being and health of their employees. The Attorney General’s office has not officially responded to the letter, and an advisor to the Attorney General suggested that enforcement will either continue as planned or be pushed until CCPA revisions can be finalized. The Attorney General recently released proposed revisions clarifying the service provider exemption. One such revision would allow service providers to use personal information internally to improve their services subject to certain limitations. Fund managers should prepare for enforcement of the CCPA as planned, while awaiting a formal response from the Attorney General.

SEC Temporary Final Rule 10(c) to Address Form ID Notarization Issues. In recognition of the issues caused by the COVID-19 public health crisis for entities and individuals who require access to file in EDGAR and the requisite notarization of the authorized signature on the Form ID application required by Rule 10(b) of Regulation S-T, the SEC announced a temporary rule to allow applicants for EDGAR access to upload a signed copy of the Form ID without notarization. The temporary rule requires that within 90 days of obtaining access to EDGAR, applicants must obtain notarization of the authorized signature on a copy of the completed Form ID and upload it as correspondence to their EDGAR account.

SEC’s Office of Compliance Inspections and Examinations (OCIE) Off-Site Exams via Correspondence for Information on Firms’ Business Continuity Plans (BCP). The SEC’s OCIE has begun off-site examinations through correspondence requests for responses and documents related to firms’ written Business Continuity Plans, Pandemic Continuity of Operations Plans, and/or equivalent informal plans or guidance (collectively, “BCP”). Firms are expected to provide copies or locations of their BCPs and any firm-issued policies, procedures, guidance and other information tailored to address continuity of business operations relating to pandemics and specifically COVID-19. Additionally, the OCIE asks for written responses to questions regarding what aspects of plans have been implemented, what limitations firms have faced in their abilities to operate critical systems, whether working remotely has affected oversight of third-party vendors, whether the firms are prepared to operate remotely for several weeks (e.g. 3+) or months, if required, etc. As the economic and operational pressures resulting from COVID-19 are affecting businesses and the industry at large, firms are strongly encouraged to revisit and enhance their BCPs in light of the threats posed by significant business disruptions.

SEC Guidance Relating to Federal Proxy Rules for Annual Meetings, “Virtual” Meetings, and Presentations of Shareholder Proposals. Under state law, issuers are generally required to hold annual meetings with security holders. Issuers with securities registered under Exchange Act Section 12 are required to comply with federal proxy rules when soliciting proxy authority from their shareholders in connection with the annual meeting. These federal proxy rules include the delivery of proxy material such as definitive proxy statements and proxy cards. Under the relief, the SEC takes the position that an issuer that has mailed and filed its definitive proxy materials can notify shareholders of a change in the date, time, or location of its annual meeting without mailing additional soliciting materials or amending its proxy materials if the issuer: 1) releases a press announcement of the change; 2) files the announcements as definitive additional soliciting material on EDGAR; and 3) takes all reasonable steps necessary to inform other intermediaries in the proxy process and other relevant market participants. In regards to issuers contemplating “virtual” shareholder meetings, issuers are reminded that the ability to conduct “virtual” meetings is governed by state law and the issuer’s governing documents. Issuers intending on conducting such “virtual” meetings are expected to notify its shareholders, intermediaries in the proxy process, and other market participants with clear logistical details of how shareholders can access, participate, and vote in such meetings. Lastly, the guidance encourages issuers to provide shareholder proponents or representatives with alternative means of presenting their proposals during the 2020 proxy season. To the extent such a shareholder proponent or representative cannot present a proposal due to COVID-19, the SEC would consider this to be “good cause” under Rule 14a-8(h) to exclude the proposal for any meetings held in the following two calendar years.

SEC No-Action Relief for Consolidated Audit Trail (“CAT”) Obligations. The SEC Division of Trading and Markets is providing no-action relief for small and large broker-dealers that are required to report trade and order data for all National Market System (“NMS”) securities and over-the-counter (“OTC”) equity securities. Under Section 19(b)(1) of the Securities Exchange Act of 1934, industry members of a national securities exchange or members of a national securities association (“Members”) are required to report to the CAT, a central depository that receives data on NMS securities and OTC equity securities, among other things. Prior to this relief, broker-dealers would have been required to submit member data to the CAT by April 20, 2020. This deadline has been extended to May 20, 2020. Self-regulatory organizations (“SROs”) responsible for ensuring compliance with the CAT NMS Plan will also not take disciplinary action against their members consistent with this relief. Notwithstanding the above, broker-dealers are reminded to conduct production readiness testing and certification processes 14 days prior to reporting.

Short-Selling Bans in Austria, Belgium, France, Italy, and Spain. Under EU Short Selling Regulation, the EU member states of Austria, Belgium, France, Italy, and Spain have enacted temporary short-selling bans to prevent destabilizing trading following market decline resulting from COVID-19. Each European countries’ temporary bans vary in scope, and in particular, which stocks are regulated by each ban. Generally, the scope of the bans include prohibitions on creating or increasing net short positions and involve shares, including cash and derivative short positions. Most bans do not apply to indexed financial instruments when the shares subject to the ban represent less than 20% to 50% of the composition of the index, depending on the EU member state ban. For more information in relation to each respective ban, please see the full order of the decisions for each of the following countries: Austria, Belgium, France, Italy, and Spain.

Tax Matters. In consideration of the impacts of COVID-19, many states are passing budgets, emergency COIVD-19 supplemental appropriation and extension of certain deadlines. Please see our post for an outline of certain tax deadlines in salient jurisdictions.

Amidst Extreme Volatility Managers Must Assess Material Terms in Live Trading Agreements. Given extreme market volatility, managers must assess the deal terms governing trading agreements such as ISDA master agreements, prime brokerage agreements, and others as certain provisions and triggering events may detrimentally affect hedge funds in the midst of current market conditions. Such negotiated provisions regarding force majeure, material adverse change/effect, counterparty powers, business day determinations, business disruptions, etc. and should be reviewed in light of current market conditions. In particular, for fund managers with ISDAs in place, please read this article by Dave Rothschild, a partner of CFM.

For general questions or concerns related to impacts of coronavirus on the operations or compliance of funds and advisers, please contact us.

****

Bart Mallon is a founding partner of Cole-Frieman & Mallon LLP. Cole-Frieman & Mallon is a boutique law firm focused on providing institutional quality legal services to the investment management industry. For more information on this topic, please contact Mr. Mallon directly at 415-868-5345.

Certain tax deadlines in the following salient jurisdictions may or may not be further extended due to disruption caused by COVID-19 as of the time of this publication:

CALIFORNIA

The deadline for tax filing and payment is extended until July 15 for all individuals and business entities for the following: 2019 tax returns; 2019 tax return payments; 2020 1st and 2nd quarter estimate payments; 2020 LLC taxes and fees; and 2020 non-wage withholding payments.

Payroll Tax: Employers may request up to a 60-day extension to file their state payroll reports and/or deposit payroll taxes without penalty or interest by following the instructions of the Employee Development Department (EDD).

San Francisco

Businesses with less than $10 million in gross receipts may defer their first quarter business taxes (which under normal circumstances must be pre-paid by April 30th) until February 2021. The deferral is applicable to gross receipts tax, payroll expense tax, commercial rents tax and homelessness gross receipts tax.

No interest payments, fees or fines will accrue as a result of the deferral. Further details are available in the announcement from the Office of the Mayor.

No relief has been provided with respect to property tax.

Illinois has yet to announce an extension of

deadlines for tax filings and payments as of the date of this publication.

NEW YORK

On March 16, 2020, the New York State Tax

Department announced that it had not extended the deadline to file personal

income tax or other tax returns. New

York has yet to announce an extension of deadlines for tax filings and payments

as of the date of this publication.

New York has waived fines for businesses that

have missed the sales tax deadline of March 20, 2020. There is no waiver of accrued interest.

New York City

The city is in the process of establishing the Small Business Continuity Fund which intends to provide financing to businesses demonstrating at least a 25% decrease in revenue caused by COVID-19.

For general questions or concerns related to impacts of coronavirus on the operations or compliance of funds and advisers, please contact us.

****

Bart Mallon is a founding partner of Cole-Frieman & Mallon LLP. Cole-Frieman & Mallon is a boutique law firm focused on providing institutional quality legal services to the investment management industry. For more information on this topic, please contact Mr. Mallon directly at 415-868-5345.

Investment Management Firms May Be Considered Essential Financial Businesses Under Federal Guidance and State Orders.

The Cybersecurity and Infrastructure Security Agency (CISA) lists asset management as a vital component of our nation’s critical infrastructure. As the federal risk advisor, CISA created guidance to help state and local governments ensure that employees essential to operations are able to continue working. In consideration of CISA’s guidance, whether investment management firms would be considered essential financial businesses may depend upon each State’s directives. Generally, the best practice for firms moving forward is to require workers to telework or work-from-home if possible, but allow supporting personnel to continue selective operations in the office if necessary to ensure the firm’s continued operation.

CALIFORNIA

California Executive Order N-33-20 orders “all individuals living in the State of California to stay at home or at their place of residence except as needed to maintain continuity of operations of the federal critical infrastructure sectors” as outlined by CISA. As discussed earlier, asset managers are included under CISA’s guidance and should be permitted to allow supporting personnel to continue operations in their California offices.

CONNECTICUT

Connecticut Executive Order No.7H orders that “non-essential businesses or not-for profit entities shall reduce their in-person workforces at any workplace locations by 100% not later than March 23, 2020 at 8:00 p.m. Any essential business or entity providing essential goods, services or functions shall not be subject to these in-person restrictions.” The order defines “essential businesses” as those that, “include, but not be limited to, the 16 critical infrastructure sectors as defined by the Department of Homeland Security” and as outlined by CISA. Asset managers are included under CISA’s guidance and should be permitted to allow supporting personnel to continue operations in their Connecticut offices.

DELAWARE

Delaware Fourth Modification of the Declaration of a State of Emergency defines “essential businesses” as those that employ or utilize workers in financial services who support financial operations, such as those engaged in the selling, trading, or marketing of securities, those engaged in giving advice on investment portfolios, and those staffing data and security operations centers.” Under this definition, asset managers should be permitted to allow personnel to continue operations in their Delaware offices.

ILLINOIS

Illinois Executive Order 2020-10 orders that “all Essential Businesses and Operations are encouraged to remain open. To the greatest extent feasible, Essential Businesses and Operations shall comply with Social Distancing Requirements as defined in this Executive Order, including by maintaining six-foot social distancing for both employees and members of the public at all times.” Under the order, Essential Businesses are defined as including financial institutions. Accordingly, it is reasonable to take the position that asset managers should be permitted to allow personnel to continue operations in their Illinois offices.

NEW JERSEY:

New Jersey Executive Order No. 107 allows flexibility for businesses with employees that are unable to work-from-home or perform telework. In such situations, the order requires businesses to use its best efforts to allow the minimum number of workers necessary to ensure that essential operations can continue. Accordingly, it is reasonable to conclude that asset managers have the discretion to decide which, if any, personnel can continue selective operations in their New Jersey offices in order to ensure the firm’s continued operations.

NEW YORK

New York Executive Order No. 202.6 orders that employers “reduce the in-person workforce at any work locations by 100%…” with exception to “an entity providing essential services or functions.” In a release expanding on the definition of “Essential Businesses” for the purposes of Executive Order 202.6, such essential financial institutions include “services related to financial markets.” Accordingly, it is reasonable to take the position that asset managers should be permitted to allow personnel to continue operations in their New York offices.

For general questions or concerns related to impacts of coronavirus on the operations or compliance of funds and advisers, please contact us.

****

Bart Mallon is a founding partner of Cole-Frieman & Mallon LLP. Cole-Frieman & Mallon is a boutique law firm focused on providing institutional quality legal services to the investment management industry. For more information on this topic, please contact Mr. Mallon directly at 415-868-5345.

On March 27, Congress passed the $2 Trillion CARES Act, the largest financial relief bill in history, aimed at providing financial assistance to businesses and individuals to alleviate the economic fallout caused by the COVID-19 public health crisis. A core focus of the CARES Act is $350 billion in financial aid for small businesses through federal loans under a new Small Business Administration (“SBA”) loan program called the Paycheck Protection Program (the “PPP”). The highlights of the program for qualifying businesses include the following:

Eligibility. Eligible businesses include any business that already meets the applicable regulations to constitute “small business concerns” under the Small Business Act, businesses with up to 500 employees, non-profit organizations, businesses in the accommodation (lodging) and food services businesses with no more than 500 employees at each location, and eligible sole proprietorships and independent contractors.

Terms. An eligible business can borrow 2.5 times their monthly payroll costs, up to $10 million. “Payroll costs” includes salaries, wages, paid sick leave, health insurance premiums, retirement benefits, tips, state and local taxes on employee compensation, but does not include compensation to any individual employee or independent contractor in excess of $100,000.

Permitted Uses of Proceeds.Businesses may use PPP proceeds for the following business expenses: payroll costs (as defined above), rent, utilities, and interest payments on any mortgage or debt obligations incurred before February 15, 2020, excluding payments or prepayments of principal.

Loan Forgiveness. Borrowers may apply for loan forgiveness in an amount equal to funds used to pay eight weeks of payroll costs, mortgage interest, rent and utilities starting from the date of such Borrower’s PPP loan. The amount of loan forgiveness available is limited to the principal amount loaned under the PPP loan. Furthermore, in an effort to incentivize businesses to keep employees and maintain salaries or wages, the amount of loan forgiveness available is subject to reduction if the Borrower’s average number of full-time employees during the eight week period is lower than the average number of full-time employees in the 12-month period prior, or if there is a 25% reduction of the total salaries or wages of such employees during the eight week period. The 25% reduction guideline does not apply to employees whose annual salary or wages for any pay period in 2019 was greater than $100,000. An exemption from the reductions in loan forgiveness applies if the Borrower had reduced employees or salaries or wages as a result of the COVID-19 pandemic, but eliminates such reduction by rehiring the laid off employees or increasing salaries or wages to prior levels by June 30, 2020.

The highlights of the CARES Act is intended to be a summary of the over 800 page relief bill. The CARES Act is subject to change over time during the legislative process. For questions or concerns related to impacts of coronavirus on the operations or compliance of funds and advisers, please contact us.

****

Bart Mallon is a founding partner of Cole-Frieman & Mallon LLP. Cole-Frieman & Mallon is a boutique law firm focused on providing institutional quality legal services to the investment management industry. For more information on this topic, please contact Mr. Mallon directly at 415-868-5345.

Managers Should Be Aware of Additional Termination Events

By David Rothschild

At this time of extreme market volatility, it is critical for managers with ISDA Master Agreements (“ISDAs”) in place to understand the NAV Trigger Additional Termination Events described in their ISDAs, and what actions to take if they trip one.

As quick background, the Schedule to almost every ISDA Master Agreement to which a hedge fund is party will include an Additional Termination Event (“ATE”) pegged to a specific percentage decline in the fund’s net asset value over various periods (usually monthly, quarterly and annually). Some ISDAs will also include a “NAV Floor” concept triggering an ATE any time the fund’s NAV falls below a specific value (expressed either as a dollar value, or a percentage of a prior NAV, or both). If an ATE is triggered and the dealer elects to act on it, the dealer generally has the right close out all of a fund’s open positions, a result every manager wants to avoid.

NAV Trigger ATEs are among the most heavily-negotiated provisions in a hedge fund’s ISDA, and the specific figures for the monthly, quarterly and annual triggers, as well as NAV Floor provisions, will differ from fund to fund. What some managers may not realize is that the language describing these calculations and when they must be performed may also differ. Ideally, your NAV Trigger ATEs will be “point-to-point” and measured only as of the last day of the month – i.e., your NAV on the last trading day of a month is compared to your NAV on the last trading day of the prior month, quarter or year as applicable, to determine whether you have tripped an ATE. Many ISDAs, however, will have “any day” triggers – i.e., a NAV decline on any day as compared to the prior month, quarter or year could trigger an ATE. At this point, managers should review their NAV Trigger language and consult with legal counsel if they have questions regarding when or how these calculations must be performed.

If your fund has experienced a NAV decline that triggers an ATE under your ISDA, you are obligated to formally notify the dealer of that fact. That notice to the dealer should include an explicit request for them to waive the ATE; depending on your specific facts and circumstances and your relationship with a given dealer, they may grant you a waiver. A waiver means the dealer loses the right to close out your positions as a result of that ATE.

If you negotiated your ISDA, it may also include a “fish or cut bait” provision, which essentially gives the dealer a deadline to declare an ATE after you notify them that the relevant ATE was triggered. If you have a “fish or cut bait” provision in your ISDA that applies to a NAV Trigger ATE, pay close attention to the notice procedures described therein (many dealers require multiple forms of notification to specific addresses or emails in order for the “fish or cut bait” provision to be properly invoked), and follow them exactly to put the dealer on notice and start the clock running on the time period. If you properly follow those procedures and deadline passes, the dealer loses the right to close out your positions as a result of that ATE, whether or not they grant an explicit waiver.

Of course, if you have any questions while reviewing your ISDAs or how to interpret these critical provisions, you should reach out to your legal counsel immediately.

****

David Rothschild is a partner of Cole-Frieman & Mallon LLP and routinely focuses on ISDA matters. Cole-Frieman & Mallon is a boutique law firm focused on the investment management industry. For more information on this topic, please contact Mr. Rothschild directly at 415-762-2854.

Thank you to everyone who attended our bitcoin mining panel last week. We had a fantastic audience with many questions for our panel of bitcoin mining experts – Mathew D’Souza of Blockware Solutions, Thomas Ao of MCredit and Yida Gao of Struck Capital. The panel lasted just over one hour and was ably moderated by Michael Fitzsimmons of Williams Trading and was sponsored by Cole-Frieman & Mallon LLP and Aspect Advisors LLC.

Here is the presentation with slides referenced below:

Many opportunities for BTC mining – there are many different businesses in the mining space including: direct mining, buying/selling mining rigs, making loans backed by mining rigs, developing a mining farm, and cloud mining, among others.

Potential for high returns – successful mining enterprises can make 8-12% ROI per month when BTC is priced around $10,000. (The panel focused mainly on the economics of BTC mining and did not touch on the mining of other crypto assets.)

Large secondary market for mining rigs – because it is relatively difficult to import mining rigs to the US (time and cost/tariffs), some groups buy and sell rigs on the secondary market in the US in addition to directly mining BTC and this can be a profitable strategy in its own right. Bitmain is the main supplier of new rigs and the prices from both Bitmain and the secondary market can be as volatile as the BTC market.

Cost of producing BTC – the cost to produce one BTC can vary widely depending on cost of electricity and the type of rig used, as the proprietary research from Blockware Solutions demonstrates (see attached presentation). Blockware’s research also shows that most rigs coming online are the more efficient next generation machines.

The Halvening – in May the halvening is expected to bolster the generally bullish BTC trend we’ve seen in 2020. This will undoubtedly impact the economics of mining and the secondary market for rigs.

China and mining – a favorable tax regime and lower electricity costs made China a popular location for mining, despite risks associated with the government’s stated aim to eliminate virtual currency mining as an industry. These risks have significantly abated after the recent announcement by the National Development and Reform Commission of China (NDRC) that mining has been removed from the elimination list.

Environmental impact – innovation in rig/chip designs are making mining more environmentally friendly as less watts are required per terahash. The panel generally believes that after the halvening less efficient miners will go offline.

Issues – there has been many scams with respect to mining, especially mining farms and cloud mining. Also, there is high general investment risk in mining operations because many operators just don’t know what they are doing.

Other BTC financial products – miners may decide to hedge their BTC exposure through OTC products, but in general miners are not concerned with BTC financial products unless they affect the demand/price of BTC.

We hope you enjoyed this event and if you have any feedback,

we would love to hear it in our quick

survey. Please feel free to forward this email along to anyone you

think might be interested. We look forward to seeing you at our next

event.

Regards,

Bart Mallon & Michael Fitzsimmons

Aspect Advisors LLC

Aspect Advisors LLC is a modern regulatory consultant providing customized compliance solutions to entrepreneurs. The firm has a focus on fintech companies, broker-dealers, and investment managers (hedge fund, VC, PE, RIA, etc). We provide compliance and back-office solutions engineered to decrease worry and save time and resources. Among other items, the firm helps clients with regulatory registration, drafting compliance policies and procedures, conducting annual reviews, and other bespoke items.

Cole-Frieman & Mallon LLP

Cole-Frieman & Mallon LLP is a premier boutique investment management law firm, providing top-tier, responsive, and cost-effective legal solutions for financial services matters. Headquartered in San Francisco, Cole-Frieman & Mallon LLP services both start-up investment managers, as well as multi-billion-dollar firms. The firm provides a full suite of legal services to the investment management community, including hedge fund, private equity fund, venture capital fund, mutual fund formation, adviser registration, counterparty documentation, SEC, CFTC, NFA and FINRA matters, seed deals, hedge fund due diligence, employment and compensation matters, and routine business matters. The firm also publishes the prominent Hedge Fund Law Blog, which focuses on legal issues that impact the hedge fund community. For more information, please visit us at colefrieman.com.

****

Bart Mallon is a founding partner of Cole-Frieman & Mallon LLP. Cole-Frieman & Mallon has been instrumental in structuring the launches of some of the first digital currency-focused hedge funds. For more information on this topic, please contact us or you can call Mr. Mallon directly at 415-868-5345.

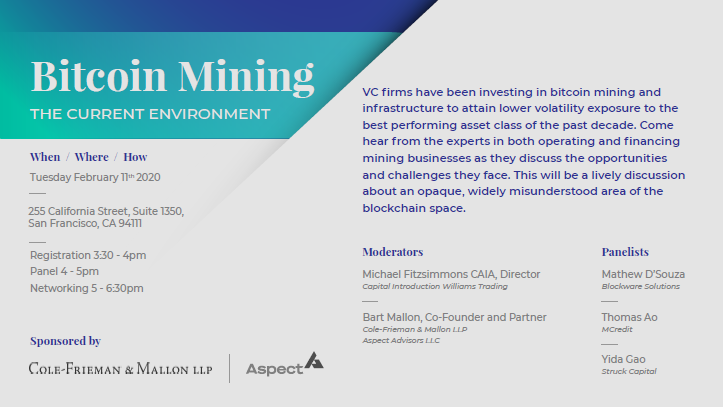

As the price of bitcoin (and other digital assets) rises, the economics of mining changes – we plan to have an event to explore the economics of mining and other aspects of the industry including any digital asset compliance matters. Below is the invitation. If you are interested in attending or would like to see the notes on the event, please contact us.

****

Please see

attached an invitation to attend a discussion on the current environment for

bitcoin mining. This event is presented by Michael Fitzsimmons of

Williams Trading and sponsored by Cole-Frieman & Mallon LLP and

Aspect Advisors LLC.

This event will

feature the following panelists:

Mathew

D’Souza of Blockware Solutions

Thomas

Ao of

MCredit

Yida

Gao of

Struck Capital

Location is at Cole-Frieman & Mallon LLP offices – 255 California Street, Suite 1350.

****

Bart Mallon is a founding partner of Cole-Frieman & Mallon LLP. Cole-Frieman & Mallon has been instrumental in structuring the launches of some of the first digital currency-focused hedge funds. For more information on this topic, please contact us or you can call Mr. Mallon directly at 415-868-5345.

We wanted to take this opportunity to thank everyone who attended and participated in our 2020 compliance update with Justin Schleifer (Aspect Advisors) and Bart Mallon (Cole-Frieman & Mallon). We understand that compliance sometimes feels like an obligation. Still, we think that our discussion last week touched on many important items for financial industry professions to keep top of mind in this new year and new decade.

We have attached a copy of the presentation to this email. Please feel free to forward along to anyone who might be interested. Some high points included:

High level trends influence how the modern investment manager interacts with compliance. Trends include the ongoing bull market, the movement of investment dollars from public investments (via IPO) to private markets, and the emergence of technology/ fintech. While these are distinct trends that need to be acknowledged, traditional compliance concepts still apply to managers although the concepts may be deployed or utilized in a different way than before.

Regulation Best Interest (“Reg BI”) will have an impact on the investment management industry in 2020. Broker-dealer and IA firms will scurry to meet the Reg BI implementation deadline. The effects will be felt more keenly by broker-dealers as they revise their practices to account for the updated fiduciary standards. Asset managers will need to address the regulation through a new Form CRS (sometimes referred to as ADV Part 3).

Privacy is paramount. There is general momentum toward consumers craving privacy. Governments and regulators are taking baby steps but are expected to do more in the future – we see that things such as the California Consumer Privacy Act and GDPR have already begun to influence the operations of many investment management companies. While managers should always maintain fundamental compliance records, there will be changes in the way that investor and customer data is ultimately accessed and available. It is therefore important for managers to stay up to date with those advances and any accompanying compliance processes.

Technological innovation (in both traditional and digital asset markets) is stretching the regulators’ ability to keep up. Regulators have trouble attracting talent to head new divisions to deal with technological innovation. Accordingly, money managers and entrepreneurs utilizing new technologies will need to understand the necessity of being able to explain the use of technology to regulators.

Access to new capital? The industry is always looking for ways to get new investors involved. A new accredited investor standard has been proposed but is not likely to significantly expand the pool of potential accredited investors and thus capital available for investment. Similar initiatives to broaden the distribution of investment products or management to a broader base of end investors (such as Regulation CF, Regulation A+, and 506(c) general solicitation) have seen generally middling to poor results for various reasons.

Information Security/Cybersecurity will continue to be a big regulatory focus and focus on this area is a business best practice. Larger firms will outsource to high tech IT firms or bring IT talent in-house. Smaller firms have many basic tools at their disposal and should focus on vendor management and selection, employee training, access to information, and other pivotal ways to increase security (2FA, using non-public wifi, port blockers, screen protectors, etc).

Taking humans out of investment management. Many investment management companies are creating organizations to bring services to the masses; these companies scale to limit human involvement. Questions on how to deal with compliance on a larger scale naturally emerge. The integration of technology (including with outside compliance vendors) becomes a key focus and commensurately decreases the reliance on human capital.

Other smaller trends have emerged. The focus on private markets is expected to heat up, not decrease (WeWork notwithstanding). Firms will continue to expand with sophisticated financial services, tools, investment strategies, different products, and new market participants, especially as millennials begin investing and saving more. As technology improves lower-fee products proliferate; many firms charge very low management fees and rely more on performance fees.

We look forward to seeing you again at a panel event in the future and wish you the best during this first quarter.

Regards,

Bart Mallon & Justin Schleifer

Aspect Advisors LLC

Aspect Advisors LLC is modern regulatory consultant providing customized compliance solutions to entrepreneurs. The firm has a focus on fintech companies, broker-dealers, and investment managers (hedge fund, VC, PE, RIA, etc). We provide compliance and back-office solutions engineered to decrease worry and save time and resources. Among other items, the firm helps clients with regulatory registration, drafting compliance policies and procedures, conducting annual reviews, and other bespoke items.

Cole-Frieman & Mallon LLP

Cole-Frieman & Mallon LLP is a premier boutique investment management law firm, providing top-tier, responsive, and cost-effective legal solutions for financial services matters. Headquartered in San Francisco, Cole-Frieman & Mallon LLP services both start-up investment managers, as well as multi-billion-dollar firms. The firm provides a full suite of legal services to the investment management community, including hedge fund, private equity fund, venture capital fund, mutual fund formation, adviser registration, counterparty documentation, SEC, CFTC, NFA and FINRA matters, seed deals, hedge fund due diligence, employment and compensation matters, and routine business matters. The firm also publishes the prominent Hedge Fund Law Blog, which focuses on legal issues that impact the hedge fund community. For more information, please visit us at colefrieman.com.

****

Bart Mallon is a founding partner of Cole-Frieman & Mallon LLP. Cole-Frieman & Mallon has been instrumental in structuring the launches of some of the first digital currency-focused hedge funds. For more information on this topic, please contact Mr. Mallon directly at 415-868-5345.